In light of the recent downturn in the FTSE 100 and FTSE 250 indices, driven by weak trade data from China and declining commodity prices, investors are increasingly cautious about market conditions. However, even amid such volatility, high-growth tech stocks in the United Kingdom present compelling opportunities for those seeking robust potential returns.

Top 10 High Growth Tech Companies In The United Kingdom

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| STV Group | 13.15% | 46.78% | ★★★★★☆ |

| Altitude Group | 23.46% | 27.56% | ★★★★★☆ |

| Filtronic | 21.83% | 33.45% | ★★★★★★ |

| YouGov | 14.31% | 29.79% | ★★★★★☆ |

| Redcentric | 4.89% | 63.79% | ★★★★★☆ |

| LungLife AI | 100.61% | 100.97% | ★★★★★☆ |

| Trustpilot Group | 16.23% | 31.98% | ★★★★★☆ |

| IQGeo Group | 11.49% | 63.61% | ★★★★★☆ |

| Beeks Financial Cloud Group | 24.63% | 57.95% | ★★★★★☆ |

| Vinanz | 113.60% | 125.86% | ★★★★★☆ |

Click here to see the full list of 46 stocks from our UK High Growth Tech and AI Stocks screener.

Underneath we present a selection of stocks filtered out by our screen.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Tracsis plc, with a market cap of £209.33 million, provides software and hardware solutions as well as data analytics/GIS services for the rail, traffic data, and transportation industry.

Operations: The company generates revenue through two primary segments: Rail Technology & Services (£34.59 million) and Data, Analytics, Consultancy & Events (£44.80 million).

Tracsis, a UK-based tech firm specializing in software and AI solutions for transportation, has demonstrated exceptional earnings growth of 99.1% over the past year, significantly outpacing the industry average of 19.9%. The company’s R&D expenses have been instrumental in driving innovation, with a focus on enhancing their SaaS offerings to ensure recurring revenue streams. Forecasts indicate that Tracsis’s earnings will grow at an impressive annual rate of 40.6%, while its revenue is expected to rise by 6.3% per year, surpassing the broader UK market’s projected growth rate of 3.7%.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Informa plc operates as an international events, digital services, and academic research company in the United Kingdom, Continental Europe, the United States, China, and internationally with a market cap of £11.02 billion.

Operations: Informa generates revenue through four primary segments: Informa Tech (£426.70 million), Informa Connect (£630.20 million), Informa Markets (£1.67 billion), and Taylor & Francis (£636.70 million). The company operates across various regions, including the UK, Continental Europe, the US, and China.

Informa, a major player in the UK tech sector, is projected to see earnings grow by 21.5% annually over the next three years, outpacing the broader UK market’s expected growth of 14.4%. Despite a challenging past year with an 11.3% decline in earnings due to a one-off loss of £213.5 million, the company’s revenue is forecasted to increase by 6.7% per year, surpassing the UK’s average market growth rate of 3.7%. Notably, Informa has repurchased 41.67 million shares for £338.9 million between January and June 2024, demonstrating strong confidence in its future prospects and shareholder value enhancement strategies.

R&D investments have been pivotal for Informa’s innovation trajectory; with expenses amounting to £120 million last fiscal year alone, these efforts are crucial for sustaining competitive advantage and driving future growth across its diverse business segments such as digital content and analytics services. The recent appointment of Maria Kyriacou as Non-Executive Director brings extensive leadership experience from global entertainment giants like Paramount Global and ITV Studios, potentially bolstering strategic initiatives within Informa’s media-focused divisions.

Simply Wall St Growth Rating: ★★★★★☆

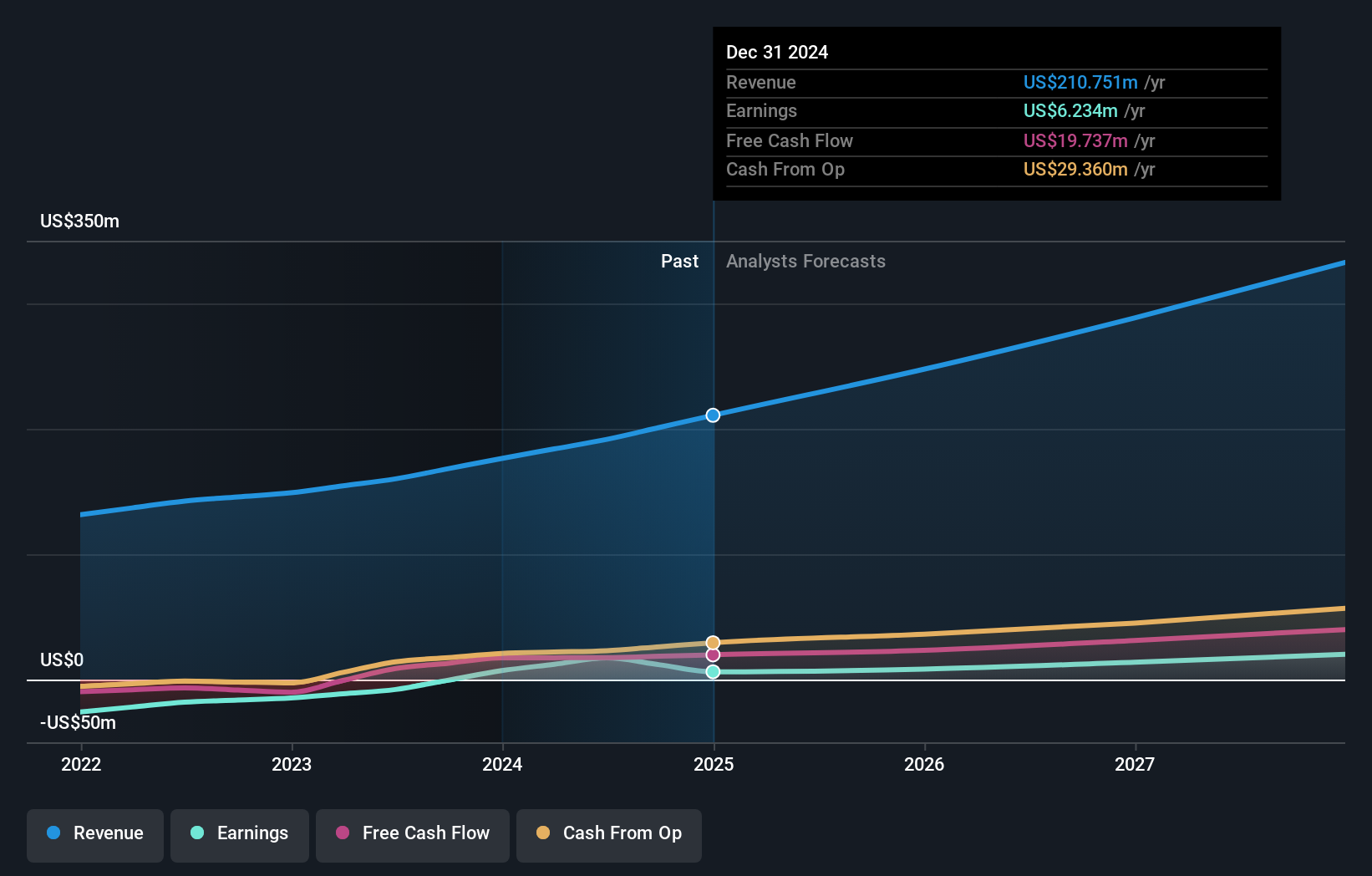

Overview: Trustpilot Group plc operates an online review platform for businesses and consumers across the United Kingdom, North America, Europe, and internationally, with a market cap of £877.35 million.

Operations: Trustpilot Group plc generates revenue primarily through its online review platform, categorized under Internet Information Providers, with a revenue of $176.36 million. The company serves businesses and consumers across multiple regions including the United Kingdom, North America, and Europe.

Trustpilot Group, a prominent player in the UK’s tech sector, has seen its earnings grow significantly, with forecasts predicting a 32% annual increase over the next three years. This outpaces the broader UK market’s expected growth of 14.4%. The company’s revenue is also projected to rise by 16.2% annually, surpassing the UK’s average market growth rate of 3.7%. Trustpilot’s R&D expenses have been substantial; last fiscal year alone saw an investment of £12 million in innovation efforts aimed at enhancing their platform and services. Additionally, recent M&A rumors involving Trafalgar Acquisition S.a.r.l.’s intention to sell up to approximately 12.5 million existing ordinary shares highlight ongoing strategic movements within the company’s shareholder base.

Seize The Opportunity

- Click here to access our complete index of 46 UK High Growth Tech and AI Stocks.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Streamline your investment strategy with Simply Wall St’s app for free and benefit from extensive research on stocks across all corners of the world.

Looking For Alternative Opportunities?

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Tracsis might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com